Year End Tax Planning - 2022

These important tax and financial planning moves can help prepare you for the upcoming tax season and better align your finances with your short- and long-term goals.

Key Takeaways

While tax and financial planning should take place all year long, there are several actionable strategies to consider before year-end deadlines.

Important life events can have financial implications and should be discussed with your tax and financial advisor.

Certain investments generate more taxable distributions than others, so work with your advisor and tax professionals to evaluate your investments and after-tax returns.

Introduction

As the war broke out in Eastern Europe this year, the physical destruction and the effects of sanctions caused additional shocks to an economy recovering from a global pandemic. We are seeing higher energy prices and weaker confidence in the economy and financial markets as the world still suffers from pandemic-driven inflation. Such has been speculated in the past few years, there has been much discussion about income tax increases in future years to recover pandemic costs. Whether those increases result in changes to capital gains inclusion rates, personal tax rate increases, adjustments to the principal residence exemption, corporate tax rate increases, or some other tax measures to target extreme wealth inequality, no one can predict the future with any certainty. The information contained in this document is accurate at the time of writing (October 2022), and the Canadian government may introduce new tax measures before the end of the year.

Despite the uncertainty of future tax policies, taxpayers can take actions based on the tax legislation in place today before federal and provincial governments introduce changes. With deadlines fast approaching, now is the time to take advantage of tax-deferred growth opportunities, tax advantaged investment strategies, and charitable-giving opportunities, among others, to maximize deductions and credits for your tax situation. Reviewing your investments in light of your goals, the tax policy environment, and the economic landscape can help you and your advisor see where adjustments need to be made to position yourself for 2023 and beyond.

Gather Information for Year-end Investment Tax Planning

- Review year to date realized gain/loss portfolio statements to estimate your expected net taxable gains or deductible losses for 2022.

- Analyze unrealized gain/loss portfolio statements of current holdings to consider triggering gains or losses in 2022 or deferring to future years.

- Obtain recent account statements with year to date taxable investment income to estimate any income taxes due in excess of your withholding taxes and quarterly tax instalments.

- Obtain recent account statements with year to date investment management fees and interest to estimate income tax deductions.

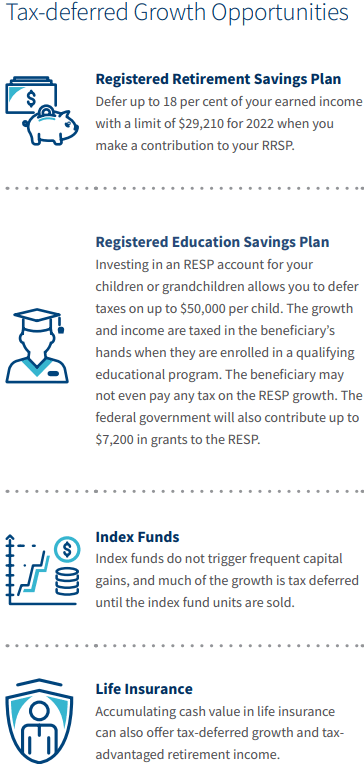

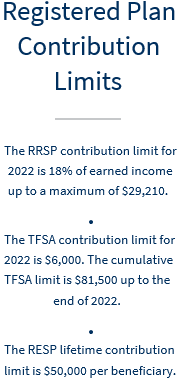

- Calculate your total RRSP contributions to employer, bank, and brokerage accounts to ensure you did not contribute in excess of your 2022 RRSP contribution room. Review against your 2021 CRA Notice of Assessment RRSP available contribution room for 2022, not the RRSP deduction limit for 2022. Withdraw excess contributions immediately to stop penalties from accruing further. Consider maximizing RRSP contributions to reduce current or future taxes and earn tax-deferred investment income.

- Calculate your total year to date TFSA contributions during 2022 to ensure you did not contribute in excess of your 2022 TFSA contribution room. Withdraw excess contributions immediately to stop penalties from accruing further. Consider maximizing TFSA contributions to earn tax-free investment income.

- Calculate your total year to date RESP contributions during 2022 to maximize annual Canada Education Savings Grants (CESG) for the year and any grant entitlements carried forward.

- Calculate your total year to date RDSP contributions during 2022 to maximize annual Canada Disability Savings Grants (CDSG) for the year and any grant entitlements carried forward.

Moves to Consider

Here are important items to think about in each of the major planning categories. Keep in mind the ideas listed here are conversation starters for most investors. You and your advisor should determine next steps for your own situation.

Income Tax Planning

- Consider loaning investment funds to your spouse at the prescribed interest rate to split investment income if one spouse earns significantly more taxable income than the other.

TIP: The CRA prescribed rate for spousal loans recently increased to three per cent and could increase in future quarters. Although less favourable with the increased rate, the three per cent interest rate will still be able to provide income-splitting benefits if the investment returns on the loan proceeds are expected to exceed three per cent. Also consider using a prescribed rate loan to split income with your children using a family trust.

- Consider exercising employer stock options in 2022 if you expect your personal tax rates to increase. The federal government enacted a new tax measure to limit the 50 per cent stock option deduction for large company stock options granted after June 30, 2021. The new rule imposes a $200,000 annual vesting limit based on the value of the option’s underlying shares at grant date.

- Complete TFSA withdrawals by December 31, 2022 to restore TFSA contribution room on January 1, 2023. If you require funds from your TFSA or want to rebalance the holdings by withdrawing securities in kind, make the withdrawal before December 31, 2022 rather than in 2023 to ensure the withdrawal value is added back to your contribution room. Asset values withdrawn in 2022 can be replaced as of January 1, 2023.

TIP: Rebalance your TFSA holdings by contributing income-producing Canadian securities “in kind” into your TFSA. Any accrued capital gains will be taxable using the value at the contribution date. Capital losses are not claimable. Therefore, do not contribute securities in a loss position to your TFSA.

- Ensure every family member age 18 and over has maximized contributions to their TFSA account.

TIP: The highest income earner can split income by gifting funds to each eligible family member to open their own TFSA account and contribute the maximum amounts. The cumulative maximum to the end of 2022 is $81,500 for individuals who were 18 years of age and older in 2009. There is no attribution on TFSA income if the funds are gifted because the income earned is tax-free. Withdrawals from and income earned inside a TFSA do not affect income tested benefits such as OAS and GST/HST credits.

Note: The TFSA account holder must be 18 years of age or older and a Canadian resident to receive TFSA contribution room each year. Age of majority for the province of residence is required to open an investment brokerage TFSA.

- Open a registered disability savings plan (RDSP) if you or your child qualifies for the disability tax credit. The federal government will match 100 per cent to 300 per cent of the contributions made to an RDSP depending on the level of family income, up to a lifetime maximum of $90,000 in total grants. The lifetime contribution maximum is $200,000 per beneficiary, and the income and growth are tax deferred.

- Talk to your employer about deducting home office expenses. With many employees working from home during the pandemic, your employer may provide Form T2200 so that you may deduct certain home office expenses. The current legislation requires your employment contract to stipulate that you are responsible for paying your own home expenses. The Canada Revenue Agency (CRA) will extend the temporary flat-rate method that allows eligible employees to deduct $2.50 for each home workday totaling $500 in 2022.

Planning for New Tax Legislation

- The First Home Savings Account (FHSA) will be available to Canadian residents who are 18 years of age or older and have not owned a home in the year the account is opened or the preceding four calendar years. The annual tax contribution limit is $8,000 up to a lifetime contribution maximum of $40,000. Like other plans, unused contribution room for the FHSA carries forward. The plan must be closed after 15 years from first opening an FHSA or when the individual turns age 71, whichever is earlier. This newly introduced savings account shares tax attributes with the existing RRSP and TFSA. Similar to RRSP, contribution to the plan is tax deductible. Similar to TFSA, incomes generated (including capital gain on the sale of the investments) are tax-free if the fund is used towards the purchase of a qualifying home.

- To be introduced in 2023, the Multigenerational Home Renovation tax credit will be available to families who renovate their home to add accommodation for a senior or disabled relative to live with them if they are eligible. The taxpayer can claim 15 per cent of up to $50,000 of the eligible renovation expenses, which means they can receive up to $7,500 refundable tax credit.

- During the election, the Liberals proposed a new minimum tax to require individuals with taxable income in the top income tax bracket to pay at least 15 per cent federal tax on taxable income. Without any further details on this proposal, the government likely intends to capture more tax beyond the existing tax minimization planning to limit significant deductions and credits, such as charitable donations, dividend tax credits, and medical expense credits. Taxpayers who plan to claim the lifetime capital gain exemption should also consider to defer the capital gain realization in multiple years.

- Consider renting out your property if you are a foreign owner of Canadian residential real estate to avoid the underused housing tax. Starting in 2022, the government implemented a national annual one per cent tax on the value of non-resident, non-Canadian owned residential real estate that the government considers vacant or underused starting January 1, 2022. Non-resident property owners should also take note of any empty homes taxes imposed at the municipal and provincial levels. For example, the B.C. government has implemented a two per cent tax on the value of the property for non-resident, non-Canadian owned residential real estate.

Investment Tax Planning

- Review your portfolio’s tax efficiency. Simply put, tax efficiency is measured by how much of an investment’s return remains after taxes are paid. Certain investments generate more taxable distributions than others. Consider rebalancing your portfolio to include more tax-advantaged investments such as Canadian dividend-paying shares and investments that allocate capital gains, especially in higher tax brackets. Work with your advisor to evaluate your investments and after-tax returns.

TIP: When rebalancing, consider using new money coming into the account versus selling off certain investments to avoid incurring unnecessary capital gains taxes.

- Review your tax-efficient placement of foreign investments between your investment, TFSA, and retirement accounts. Ensure your TFSA accounts do not hold investments that are subject to foreign withholding tax, which eliminates the tax- free benefit of the TFSA account. Consider holding certain dividend-paying foreign securities outside your RRSP/RRIF accounts if the income is subject to withholding tax. That is because the dividend will be taxed a second time upon withdrawal from the plan. Ensure lower treaty withholding rates are applied to foreign investments in your taxable investment account, where applicable.

- Work with your tax advisor to determine the best time to realize capital gains and/or harvest capital losses. Consider offsetting investment gains with losses, as appropriate, to reduce your overall tax liability. If you expect capital gains tax rates to increase in the future, consider deferring loss realizations to future taxation years. Be aware of “superficial loss” rules that stop you from deducting capital losses on the sale of a particular security if you initiate a similar position within a 61-day period (30 days before the sale date and 30 days after the sale date). The rules apply across your portfolios and your spouse’s, in both taxable and non- taxable accounts. For example, you cannot liquidate a position in one account and establish a similar position in your RRSP and expect to claim a loss.

TIP: Use the superficial loss rules to transfer a capital loss upon disposition to a spouse by having the spouse purchase the same security within 30 days of the disposition. As long as the purchasing spouse holds the security for at least 30 days, the capital loss will be denied to the selling spouse and added to the adjusted cost base of the purchasing spouse.

Financial Planning

While each individual’s needs are unique, many people have similar planning objectives – whether to ensure they have the income they need today to plan for retirement tomorrow or to grow their assets.

- Review your asset allocation to ensure it is still geared toward your goals and tolerance for risk. Risk tolerance may change based on your net worth, age, income needs, financial goals, and various other considerations. Review your holdings and your overall asset allocation then make adjustments and rebalance as necessary. Don’t forget to do this for your company-sponsored retirement accounts, too. “Set it and forget it” shouldn’t be the default for your RRSP investments.

TIP: Some investments may be better suited for particular account types from a tax standpoint. Be sure to discuss with your tax professionals.

- If you are a trustee of inter vivos trusts, consider distributing all or most trust income before December 31, 2022 to income beneficiaries. Income retained in the trust will be subject to the top federal and provincial tax rates if not distributed or allocated out to the beneficiaries. It’s important to note, however, that decisions should be made within the boundaries of the trust’s governing instrument and provincial law. Beware of the tax on split income rules that apply to trust income originating from a related business corporation where the beneficiary did not make a contribution to the business.

TIP: If the tax on split income rules do not apply to your trust, rather than accumulating income inside the trust, distribute or allocate the income (in line with trust terms and fiduciary duties) to beneficiaries, particularly those below the basic personal exemption. This essentially shifts the income and the resulting income tax burden from the trust to the beneficiary.

NEW: Canadian trusts with no income earned or realized in the year are legislated to file an annual T3 trust tax return with the CRA for trust taxation years ending on or after December 31, 2022. Furthermore, these trusts will need to report additional information on all trustees, beneficiaries, settlors, and each person who can exert control or override trustee decisions over the allocation of income or capital of the trust. The additional information includes the name, address, date of birth, tax residence, and taxpayer identification number (e.g., SIN, TN, BN) of each party.

Some exceptions to the new reporting requirements include:

- Graduated rate estates and qualified disability trusts,

- Trusts that have been in existence for less than three months at the end of the year, and

- Trusts that hold less than $50,000 in assets throughout the taxation year, provided the holdings are confined to deposits, government debt obligations, and listed securities.

Speak to your accountant about the application of these new requirements to your trust. Raymond James clients can engage our Tax Preparation Services to prepare annual T3 trust tax returns.

Retirement Planning

- Maximize your retirement contributions to take advantage of tax-deferred growth if you are still working. Many companies allow you to arrange automatic contributions each pay period and provide employer matching contributions.

TIP: Tax-deferred growth is even more advantageous when your current marginal tax rates are higher than your expected marginal tax rates in retirement.

-

Determine if you need to convert your RRSP to a RRIF. Individuals have until the end of the year they turn age 71 to convert their RRSP accounts into a RRIF account.

TIP: Turning 71? If you are earning RRSP contribution room during 2022, consider making a 2023 RRSP contribution in December 2022 based on your 2022 earned income. The contribution in excess of your 2022 contribution room will be subject to a one per cent penalty for one month, but it will provide for an RRSP deduction in 2023 or future years. Alternatively, if your spouse is under age 71, make tax deductible spousal contributions to their spousal RRSP.

- Consider whether you are going to withdraw your non-registered investment assets, TFSA assets, or RRIF assets to fund retirement and to minimize tax and OAS claw-backs. Work with your financial/investment advisor to project a withdrawal strategy to maximize after-tax wealth over your lifetime.

TIP: Consider converting a portion of your RRSP to a RRIF starting at age 65 to take advantage of the pension income credit that shelters $2,000 of pension income from federal tax if you have no other pension income.

- Evaluate the benefit of CPP sharing and maximize pension income splitting. Spouses who are both at least 60 years of age can apply to share their CPP to split income evenly. Couples can also elect to split up to 50 per cent of pension income on their personal tax returns to take advantage of the pension credit. The ability to split pension income depends on the type of pension income and whether the pension earner is under the age of 65, is 65, or older.

TIP: Discuss the pros and cons of taking CPP early with your financial/investment advisor and planning professional.

- Claim home accessibility renovations. Seniors 65 years of age or older can claim a federal tax credit equal to 15 per cent of eligible home renovation expenses ($10,000 maximum), which improve access, mobility, and functionality within the dwelling. Individuals eligible for the federal disability tax credit may also claim home accessibility renovation expenses at any age. Certain provinces may also grant a similar credit against provincial taxes.

Education Planning

- Explore your education funding options, which include Registered Education Savings Plan (RESP) accounts and In Trust for Minor accounts, which both offer flexible investment options. Consider establishing an RESP account if you haven’t already done so, and contribute a minimum of $5,000 before year-end to receive the maximum grant for the current and prior year ($1,000) from the federal government. Raymond James clients have access to all of the available provincial grants. Starting early and saving often is always a good bet.

TIP: British Columbia offers an additional $1,200 training and education savings grant for RESP beneficiaries born after 2006, and no matching contributions are required to obtain the grant. Quebec offers an additional 10 per cent grant up to $250 per year with a lifetime maximum of $3,600.

- Superfund your RESP account to maximize tax-deferred growth over the life of the RESP. Take full advantage of the $50,000 lifetime contribution limit if you can fully fund the account now. If the growth is compounded for 18 years, the increase in the value of the account will most likely exceed the foregone grants.

TIP: A one-time $50,000 contribution made at age one will grow to $121,534 by age 18 at a five per cent rate of return. Compare that balance to annual contributions of $3,125 from age one to 16, which would only equal $98,333 by age 18, even with the maximum grants of $7,200.

- Discuss alternative ways to fund future education with your financial/investment advisor. If you have already maximized your family’s RESP contributions, consider using an In Trust for Minor account to earn capital gains income that is taxable in the minor’s hands to further reduce tax on investment income. You can also invest Canada Child Benefit (CCB) payments in an In Trust for Minor account to save for education and other expenses. The income earned from CCB payments is not attributed back to the parent for income tax reporting purposes.

- When the student is enrolled in a qualifying educational program, withdraw enough educational assistance payments (EAPs) to use up the student’s personal tax credits. There is no limit on the amount of EAPs paid out of the RESP after the first 13 consecutive weeks while they remain enrolled in a qualifying education program.

TIP: Students attending a post-secondary institution outside of Canada can receive EAPs as long as the course is at least 13 consecutive weeks.

Additional Tax Considerations for U.S. Citizens

- Consider locking in all or part of your currently available U.S. gift and generation-skipping transfer tax exemption. The $12,060,000 USD (2022) base exclusion amount is scheduled to return to $5,000,000 USD as of 2026 (indexed to inflation). Do not miss the opportunity to use the current exemption if you expect your estate to be worth more than the reduced exemption when you die.

TIP: Gifts you give to adult children are not subject to Canadian tax attribution rules, but may trigger Canadian capital gains if you give assets that have increased in value from your Canadian cost.

- Review asset valuations using U.S. cost basis calculations. The most recent tax proposals do not include an elimination of the step-up in cost basis at death. Consider revisiting your original estate plan to determine if gifting assets during your lifetime will minimize U.S. estate tax on wealth transfers.

- Consider gifting ownership of your principal residence to your non-U.S. spouse to avoid U.S. capital gains tax on the actual sale of your home. U.S. citizens can only exclude up to $250,000 USD of capital gain from U.S. income tax, unlike in Canada, which provides an unlimited capital gains exemption for a designated principal residence.

TIP: Use your remaining gift exemption to eliminate any U.S. gift tax on the transaction. U.S. citizens have $12,060,000 USD available in 2022 if they have never made any reportable gifts in the past. Lifetime gifts will reduce your estate tax exemption in effect at the time of your death.

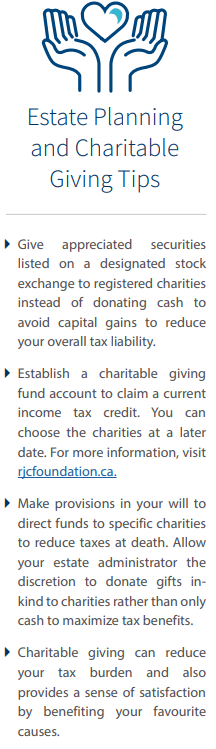

Estate Planning and Charitable Giving

Review and update estate plans and documents to reflect your current wishes. Life events such as divorce, separation, death, births, and a move to a new province or country require a review of your current estate plan. Capital properties, including shares of a private corporation, rental property, and principal residence can roll over to a spouse (or common-law partner) within 36 months of date of death at cost to avoid tax implications at death. RRIF and TFSA accounts can roll over to a spouse (or common-law partner) before December 31 of the year after the year of death if not designated as a successor. Designating your spouse as the successor rather than as a beneficiary eliminates unnecessary filings with the CRA.

- Consider making gifts to your adult children during your lifetime. These gifts will reduce the size of your estate subject to probate fees and reduce capital gains subject to disposition at death. Document the gifts to ensure they do not form part of the estate and cannot be contested. Additionally, consider reducing the RRIF balance by an additional lumpsum withdrawal before year-end unless the RRIF could be rolled to spouse or a registered disability savings plan for a financially dependent infirm child or grandchild.

- Review designated beneficiaries on registered accounts. Ensure the designations are current and your spouse is designated as the successor annuitant/holder where appropriate (on RRIFs and TFSAs). Add contingent beneficiaries in case the designated individual pre-deceases you or the account owner becomes mentally incapacitated and cannot change the beneficiaries.

- Review the legal titling on all your accounts and property to ensure they reflect your current wishes and family dynamics. Consider methods to reduce probate fees, such as joint ownership, alter-ego trusts, life insurance, and gifting assets before death.

- Give to charities close to your heart, but do so strategically to reduce your tax liability. Consider whether a trust or a Raymond James Charitable Giving Fund will help you meet your legacy and tax-savings objectives.

- Think strategically about your estate plan. Transferring assets to a living trust (inter vivos) for the benefit of your heir(s) allows you to ensure your estate distribution goes according to your desires and offers several advantages:

- Future appreciation of those assets is removed from your estate,

- Income may be shifted to beneficiaries in a lower income tax bracket,

- Transferred assets may be protected from potential creditors, lawsuits, or divorce proceedings,

- Assets held within the trust will bypass the probate process and maintain your privacy, and

- It provides for contingent management of the assets if you become mentally incapacitated and can no longer make final decisions.

Shareholders of Canadian Private Corporations

- Evaluate your salary dividend mix to minimize overall personal and corporate tax, while meeting your cash flow requirements and avoiding the punitive tax on split income rules for family member shareholders. Reasonable salaries paid to family members working in the business are not affected by the tax on split income rules.

TIP: Determine if any shareholders are affected by the tax on split income rules. Pay out capital dividends and repay shareholder loans as tax-free sources of cash. Pay out taxable dividends if your corporation has a refundable dividend tax balance (RDTOH) to recover corporate taxes. Consider the impact of any possible federal and provincial tax rate changes that affect business and investment taxable income.

- Determine how to minimize passive investment income if the corporation earns active business income. A Canadiancontrolled private corporation (and any associated companies) may be subject to significantly higher tax rates on active business income when adjusted aggregate investment income exceeds $50,000. The $500,000 small business deduction limit will be reduced by $5 for every $1 the corporation’s investment income exceeds $50,000 and will be grinded to $nil at $150,000.

TIP: Consult with your corporate tax accountant to determine the impact, if any, on active income earned inside your corporation. Key shareholders with a history of receiving salary should consider setting up an Individual Pension Plan (IPP) to shift the investments out of the corporation. Corporate-owned life insurance may also provide a solution: income from investments earned in an exempt life insurance policy is not considered to be the passive investment income for the above rules relating to the small business deduction. A life insurance policy’s premiums are paid by after-tax cash. When the corporation’s tax rate is lower than the shareholder’s personal tax rate, the cost of insurance is lower when the premiums are paid by the corporation. Furthermore, if the life insurance policy is held as collateral, the net cost of insurance paid for the life insurance is tax deductible to the corporation. Contact your financial/investment advisor to discuss investment strategies to manage investment income types earned inside your corporation.

- Review your business succession plan and the potential tax impact upon your death. Review your shareholder agreements to ensure your rights are protected and to avoid shareholder disputes after your passing. Determine whether it is an appropriate time to freeze the company in order to pass future value to your heirs. Evaluate your ability to claim the $913,630 (2022) lifetime capital gains exemption upon the sale of your small business shares or upon your death.

TIP: The passage of Bill 208 in June 2021 may provide a window of opportunity for you to pass your active businesses to your children and grandchildren to make use of your lifetime capital gains exemption. Discuss this opportunity with your corporate tax advisor as soon as possible because the federal government intends to amend the new rules to prevent unintended loopholes.

- Consider purchasing capital property for your business that is eligible for immediate expensing. Certain property acquisitions on or after April 19, 2021 that become available for use before January 1, 2024 are eligible up to a maximum amount of $1.5 million per taxation year. The limit is shared among associated members of a group of Canadian-Controlled Private Corporations (CCPCs).

Work with Your Financial/Investment Advisor

Despite what may be happening in the markets and the overall economy, there are several key actions you can take at year-end to help you get a better grasp of where you stand financially. A year-end review with your professional advisors also helps ensure you’re on track to meet your goals and helps identify areas in need of adjustment so your plan can evolve as your needs change.

Take the time now to talk about those changing needs, so you and your advisor(s) fully understand where you are and where you want to go.

These important tax and financial planning moves can help prepare you for the upcoming tax season and better align your finances with your short- and long-term goals.